Scare Tactics

Your fear of taxes is an easy target for fear marketing. You have heard the threat “you will pay away most of your retirement savings in taxes” or the promise of a “tax-free retirement.”

Why does this work?

Because you hate taxes almost as much as sneakers that aren’t white, teenage trick-or-treaters, and Costco cart traffic jams on sample day.

Your tax fear might also be your retirement Achilles’ heel. The biggest retirement mistakes are fear-based decisions.

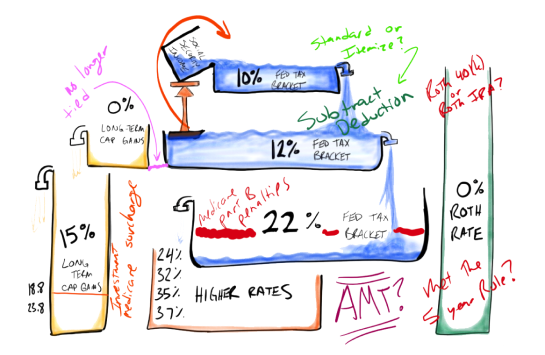

Taxes are complicated

There is no easy way around that.

If this drawing makes sense to you, you’re done reading.

No surprise, we are all still here. There are some straightforward guidelines which will help retirees navigate the tax minefield.

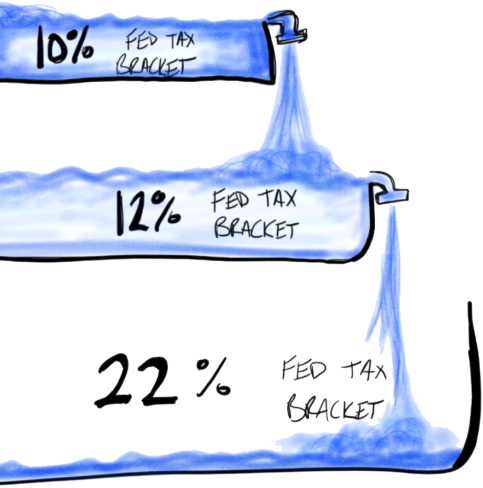

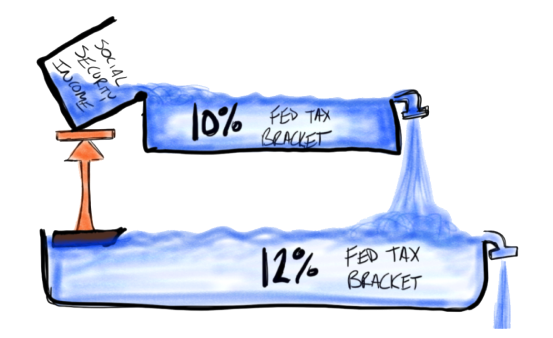

Income Bracket Waterfall

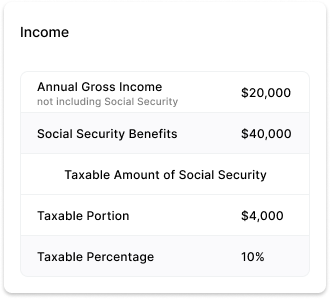

The 85 percent number is a common point of confusion. People think, “My Social Security is TAXED AT 85 percent!” No, 85 percent of your Social Security can be taxed (subject to your marginal tax rate).

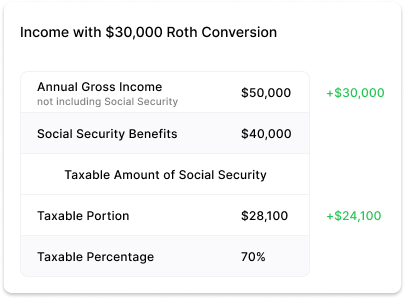

A client of mine who was familiar with the tax lines recently told me he would like to do a $30,000 Roth conversion in the 12 percent tax bracket. After all, 12 percent might be the lowest rate he sees in his lifetime. He was expecting to pay 12 percent of $30,000 in taxes ($3,600).

Adding $30,000 of additional Adjusted Gross Income (AGI) pushed the taxable portion of his Social Security from 10 percent to 70 percent. Take a look:

+$54,100 of income

+$6,104 of tax

The true tax rate would be $6,104 out of $30,000, just over 20 percent. He still decided it was worth it, however, 12 percent and 20 percent are not the same. Yet, he was “in the 12 percent bracket.”

Guideline 3 : Beware of the Social Security tax accelerator

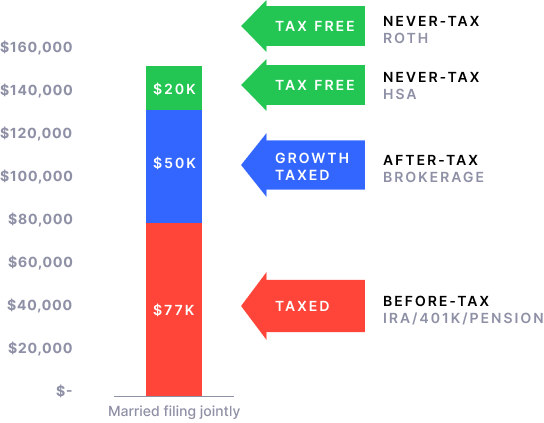

For those of you who are lucky (or strategic) enough to have filled all three tax categories, you have flexibility.

One of our engineering clients calls this “degrees of freedom.” You have the ability to withdraw from an IRA at income tax rates, sell non-retirement assets at capital gain rates, and/or withdraw from Roth at a zero percent rate.

Here is an example of someone being able to spend around $150,000 per year in retirement at a federal tax rate of roughly 8 percent. It is not magic, it is strategic planning to allow for “degrees of freedom. In other words, the flexibility to behave in different ways.

Call it “degrees of freedom,” call it “marginal tax-bracket management,” or just call it “smart thinking.” It doesn’t matter what you call it, being aware of taxes is much better than being afraid of taxes.